Last time I gave a short explanation of commercials models used in 3PL. Today I want to discuss rate cards a bit more as they are an important mechanism between customer and 3PL. Rate cards are the most commonly used pricing mechanism for 3PLs and consist of different aspects which I will further explain today. Only warehousing rate cards are explained here.

Warehouse rate cards typically consist of 2 cost drivers: variable and fixed costs.

- Variable costs: these are costs which are driven by moving product throughout the DC. Think about labour, MHE and consumables which fluctuate throughout the year as volumes increase / decrease. These costs are generated by the physical warehouse tasks we see in inbound, receiving, replenishment, picking, Value-Added Services (VAS) and outbound areas of the DC.

- Fixed costs: as the term implies, these are costs which remain fixed throughout the year. Think rental, occupancy (electrical, water usage, waste removal and other property related costs), capital depreciation, office and IT related costs which are periodically charged.

Variable rates and thus costs are connected to different volume streams within the warehouse which again relate to each main area within the warehouse.

- Receiving: mostly containers and LCL freight received from overseas manufacturers within the warehouse. Product is checked, sorted and palletised for put-away into storage.

- Returns: returned product (damaged, mis-picked or not wanted) is received, checked, assessed and then either put into quarantine or put back into stock.

- Put-away into storage: via MHE, put-away into storage media like single selective, double-deep or satellite rack.

- Replenishment: stock needs to be replenished into pick faces before it can be picked from for fulfillment. (also called decanting when stock is replenished into order totes for storage in a GTP system)

- Picking: often the most complex & labour intensive area within the warehouse. This is where order profile, pick types, order consolidation, batching & waving and many more methods come into play to pick orders as efficiently as possible.

- VAS (value adding services): some orders depending on the customer may require additional processing or special tasks to enhance the product being received by the customer. This could be gift wrapping, adding labelling or promotional material etc. These tasks can be highly complex and are often undercooked and difficult to price.

- Dispatch: this will cover essential tasks that need to be completed to dispatch the carton and will involve tasks such as packing, invoicing, labelling and closing the carton.

The above 7 main areas can consist of many different tasks and flows to support the operation. Volume increases, order profiles, storage requirements and so many other business rules will determine a suitable solution to cater for the operation. From a rate-card perspective, it is challenging to funnel all these tasks into several measurable KPI’s for pricing & reporting. What tasks go together well and what product and volumes are included in this task? And what rate should be provided which is representative of the operation while also harboring a continuous revenue stream?

Generally, rates which quantify inbound volumes, outbound volumes and storage levels (or space requirements) are used to build-up a rate card. An operation which moves predominantly full pallets will do well with a pallet in, out and pallets stored rate while E-comm operations will do better with cases in & lines out to measure activity. There is no silver bullet to give an optimal rate card, but there are indications to build rate cards in an operationally logical way. It is important that the rate card reflects the operation in the most important aspects of the operation. Simply put: if you store pallets, show it in the rate cards. If you ship lots of single unit orders (e-comm), show it in your rate card!

Fixed rates and thus costs are connected to the non-volume related aspects of warehousing which are mostly fixed. Think about operating space in the DC, storage locations, office and annual licensing fees. So which areas of the warehouse fall under fixed costs? In all honesty, each client has their own definition of fixed cost: some include MHE under this cost while this actually varies with volumes. Typically, fixed costs can be explained in the following costs:

- Storage costs: these costs are the rental costs of the warehouse and office together with the depreciation costs of the rack & pick faces to support the operation. Why also racking costs? Because if the operation grows and requires more storage, the 3PL recovers costs for that extra rack as well instead of just extra space.

- Warehouse running costs: these are all costs associated with running the warehouse every day. Think about electricity, waste removal, water, security, office & amenities, licensing fees, audits & inspections costs and more. These costs can be a combination of client specific costs (licenses, office) to costs based on space occupied within the facility.

- Depreciation costs: these are all costs for new equipment purchased within the operation written down over the life of the contract or a longer period. For example: equipment costs are depreciated over 10 years, but the customer exits prematurely after 3 years. For client specific equipment (automation, packing machines, special MHE) a balloon payment should be in place to cover the 3PL for losses on this equipment as it cannot use this for another customer as it’s specially customised equipment. All other equipment that can be re-utilised for other clients (packing tables, scrubbers, computers, label machines) will be taken over to a new account if possible.

- IT costs: think new computers, label scanners, RF guns, WMS licenses, the actual WMS, high-speed internet connection costs into the DC, security scanners and much more. IT costs are often depreciated in 3 years’ time before they need to be renewed. WMS is a different discussion altogether!

- Management costs: all costs for salaried personnel which are to manage the operation. Based on the size of a client’s operation and complexity, this does not always warrant a full-time manager. For example, account managers can service multiple accounts, therefore splitting their salary-costs over multiple accounts.

- Implementation costs: costs to implement the new operation from contract award, to Go-live to bedding-down the operation. Sometimes the 3PL doesn’t charge this cost directly and absorbs the cost for a suitable new client. Not to be taken lightly, implementation can make or break an operation and thus your fulfillment towards your customer. Nobody likes the horror-stores of Go-lives gone bad- costing lots of money and manpower hours to rectify! An experienced project manager with a good IT integration team is critical to a good implementation process.

There are always expectations of costs which do not fit in either of the drivers. Consumables (items the operation consumes on a regular basis- different box sizes, shrink-wrapping, labels etc.) are partially driven by volume but are also often required to support changes in the operation. As this can be hard to quantify and can change quickly with new requirements, it’s often charged on an ad hoc or cost + basis.

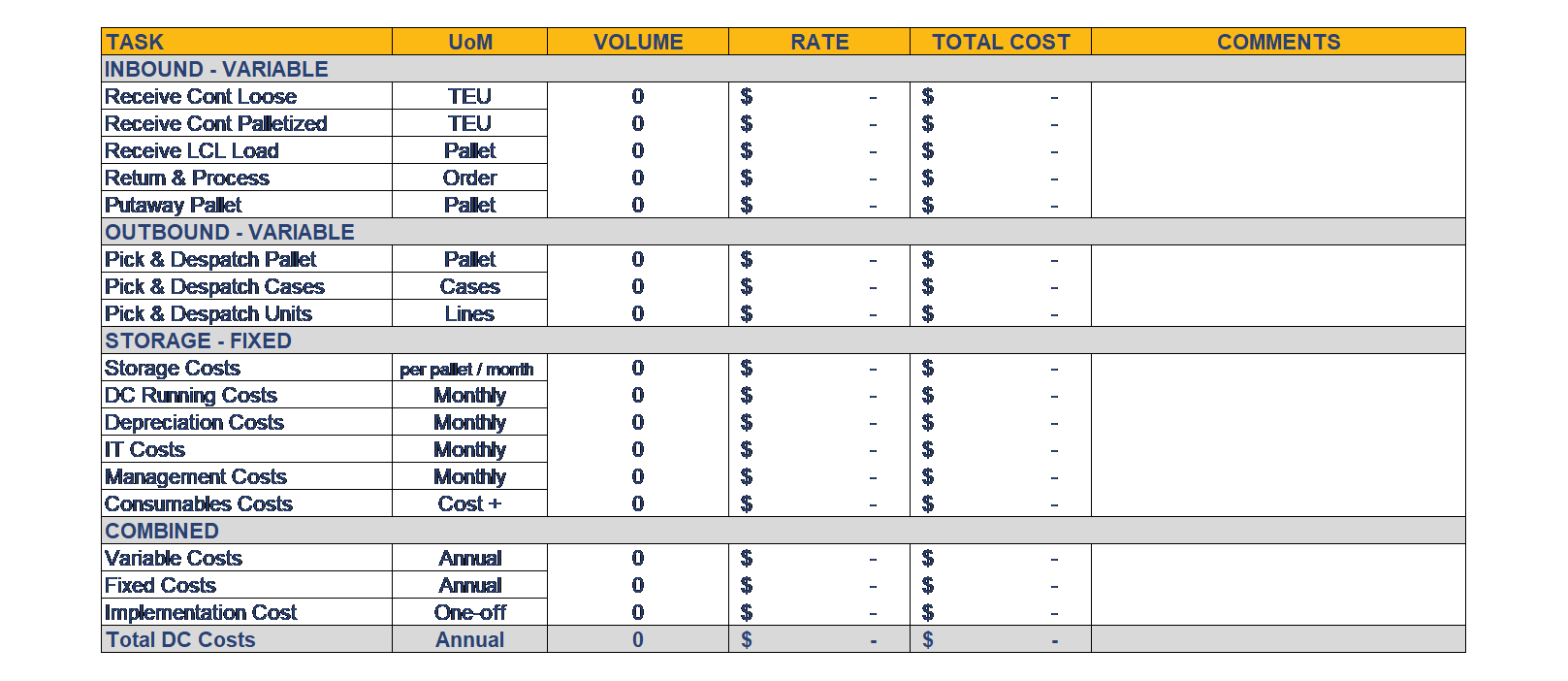

See below for an example rate card where the I’ve separated the different cost drivers with tasks and UoM. (Unit of Measure) In a next article I’ll explain on how to fill this in. Hope this gives you a better understanding of the different cost buckets which make-up rate cards.